Navigating the financial challenges of college can be daunting. Balancing tuition, books, living expenses, and social activities requires a strategic approach to budgeting. With over 20 years of experience in personal finance, I’ve seen countless students struggle with financial management. This guide aims to provide you with practical, actionable tips to help you manage your money effectively and ensure a financially secure college experience.

1. Understand Your Income and Expenses

Before you can create a budget, you need a clear picture of your financial situation. Start by listing all sources of income, such as:

- Scholarships and grants

- Part-time jobs

- Allowances from family

- Student loans

Example: If you receive $500 monthly from a part-time job and $200 from family support, your total monthly income is $700.

Next, identify your expenses, which typically include:

- Tuition and fees

- Textbooks and supplies

- Rent or dorm fees

- Groceries

- Transportation

- Entertainment

- Miscellaneous expenses (like toiletries, laundry, etc.)

Example: A typical monthly expense breakdown might look like this:

- Rent: $600

- Groceries: $200

- Transportation: $100

- Utilities and internet: $100

- Entertainment and dining out: $150

- Miscellaneous: $50

Total Monthly Expenses: $1,200

2. Create a Realistic Budget

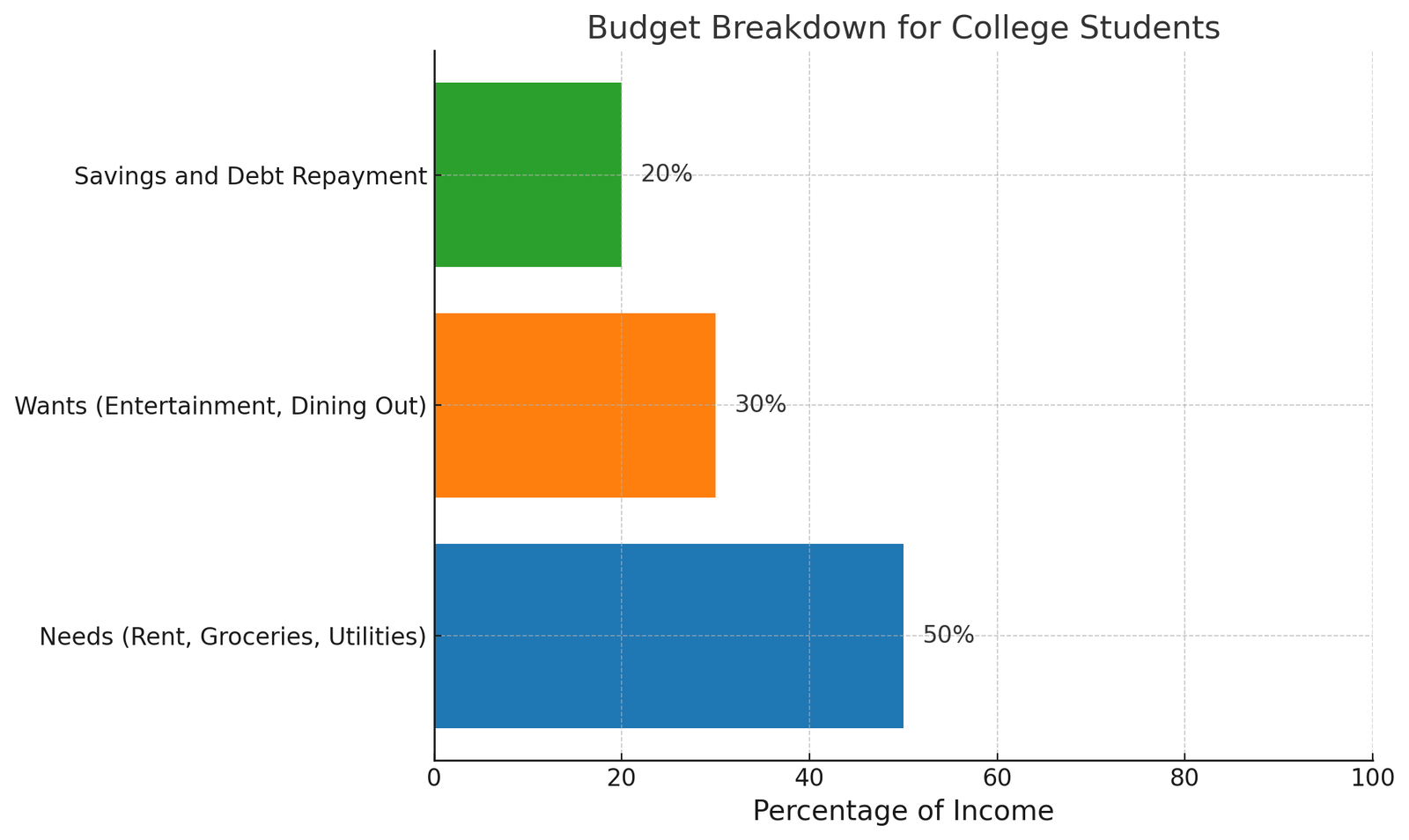

Once you understand your income and expenses, you can create a budget. Use budgeting tools like Mint, YNAB (You Need A Budget), or a simple spreadsheet. Allocate your income to cover all your expenses, ensuring you prioritize essentials like tuition, rent, and groceries. A common budgeting method is the 50/30/20 rule:

- 50% for needs (rent, groceries, utilities)

- 30% for wants (entertainment, dining out)

- 20% for savings and debt repayment

Example: With a $1,200 monthly income, allocate $600 for needs, $360 for wants, and $240 for savings and debt repayment.

3. Track Your Spending

Keeping track of your spending is crucial to sticking to your budget. Regularly review your transactions and categorize them to see where your money is going. Many banking apps and budgeting tools offer tracking features that can help you stay on top of your spending habits.

Example: If you notice you’re spending $100 monthly on coffee, consider cutting back to save money for other priorities.

4. Cut Unnecessary Expenses

Finding ways to reduce expenses can free up money for savings or unexpected costs. Consider these strategies:

- Cook at home instead of eating out.

- Use student discounts for purchases and services.

- Buy used textbooks or rent them instead of purchasing new ones.

- Use public transportation or carpool to save on gas and parking fees.

- Limit impulse purchases by making a shopping list and sticking to it.

Example: Cooking at home can save you $50-$100 per month compared to eating out regularly.

5. Build an Emergency Fund

An emergency fund is a financial safety net for unexpected expenses, such as medical bills or car repairs. Aim to save at least $500 to $1,000 initially, then gradually increase it to cover three to six months of living expenses. Start small by setting aside a portion of your income each month.

Example: If you save $20 from your income each week, you’ll have $1,040 saved by the end of the year.

6. Utilize Campus Resources

Many colleges offer resources to help students manage their finances. Take advantage of free financial literacy workshops, counseling services, and academic resources like libraries and computer labs. Additionally, explore opportunities for on-campus jobs or internships that can provide extra income and valuable experience.

Example: Attending a financial literacy workshop can teach you how to better manage your money and make informed financial decisions.

7. Plan for the Future

While it might seem early, planning for the future is essential. Consider opening a savings account or an Individual Retirement Account (IRA) to start saving for long-term goals. If you have student loans, familiarize yourself with the repayment terms and explore options for repayment assistance or forgiveness programs.

Example: By opening a high-yield savings account and depositing $50 monthly, you can grow your savings with interest over time.

Conclusion

Budgeting in college doesn’t have to be stressful. By understanding your financial situation, creating a realistic budget, tracking your spending, and making conscious decisions, you can manage your money effectively and avoid unnecessary debt. Remember, the financial habits you develop now will set the foundation for your future financial health. With these tips and a proactive approach, you’ll be well on your way to mastering your money and enjoying a financially secure college experience.